The 12 agents behind UK interest rates...

Some names you won't recognise but probably should + FTSE + Michael Lewis

4500 Parkway, 3 Science Square and Piccadilly Plaza. These addresses don’t exactly have the same ring to them as the Old Lady of Threadneedle Street. But they are playing a key role in setting Britain’s interest rates too.

These addresses are offices in Hampshire, Newcastle and Manchester for the Bank of England. They are the base for three of the Bank’s 12 agents. This network of regional agents delivers intelligence to the Bank in London through discussions with contacts and businesses. In Hampshire the agent is Andrew Holder, who used to be a research adviser to Andrew Sentance when he was on the rate-setting Monetary Policy Committee. In Newcastle it is Mauricio Armellini, who left his native Uruguay in 2004 to do an economics PhD at Durham. And in Manchester it is Alison Stuart, who grew up in Leeds, likes rugby union, cricket, football and hiking, and spent 15 years working for the International Monetary Fund in Washington.

I want to have a look today at who the Bank’s agents are but also their feedback on the economy, because this intelligence can be linked to the Bank taking a more aggressive stance on tackling inflation.

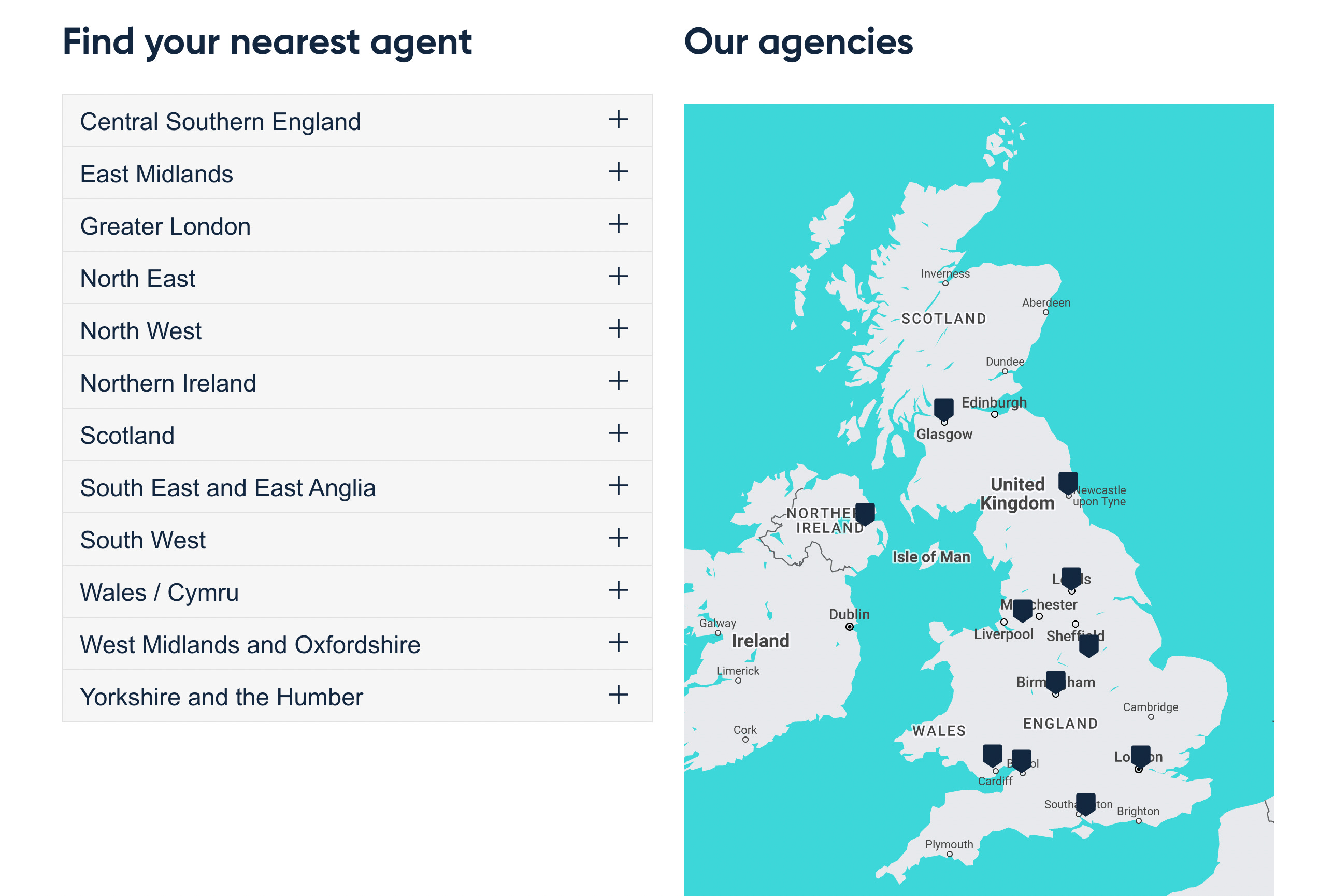

The Bank’s regional offices are led by the agent and usually one deputy agent, although the north-west England office has no deputy and some have two or three. This is how the map of the offices on the Bank’s website looks…

The bank claims its agents speak to at least 700 businesses each quarter and deliver 600 presentations a year. These agents have traditionally had a low profile – far lower than the nine members of the rate-setting MPC – but perhaps it should be much bigger. These individuals are key to connecting the Bank with what is actually going on in the economy on the ground in the UK.

Below is a list of the 12 agents. One observation I had when I looked into their backgrounds is how long they have worked at the Bank. This won’t help criticism of the organisation that it suffers from groupthink. However, Andy Haldane, the former chief executive, was also a Bank lifer and was considered a maverick thinker. There is a mix of geographic and educational backgrounds among the agents (although the south-east and Oxbridge feature heavily). Rosie Smith in Nottingham and Alex Golledge in Leeds, for instance, joined straight out of school…

Anyway, here is a list of the agents and when they joined…

Central Southern England: Andrew Holder, joined Bank in 2001 after working for Treasury

East Midlands: Rosie Smith, joined Bank in 1986 straight from school

Greater London: Rob Elder, joined 1998

North East: Mauricio Armellini, joined 2014

North West: Alison Stuart, joined 1986 then worked for International Monetary Fund between 2005 and 2020 before returning

Northern Ireland: Frances Hill, joined 2000

Scotland: William Dowson, joined 1995

South East and East Anglia: Phil Eckersley, joined 1987

South West: Malindi Myers, joined 2018, previously worked for Treasury, Office for National Statistics and European Commission

Wales: Stephen Hicks, joined 2015

West Midlands and Oxfordshire: Graeme Chaplin, joined 1992

Yorkshire and Humber: Alex Golledge, joined 1998 straight out of school

The agents’ influence is shown by the minutes from the Bank’s rate-setting meeting this week, where the MPC voted to increase rates by 0.25 percentage points to 1.25 per cent. Much of the initial reaction to the Bank’s announcement yesterday was to dismiss it as too little, too late in the fight against inflation, which is now going to exceed more than 11 per cent by October according to its own forecasts. However, financial markets think the Bank is getting more aggressive after comments in the minutes that it would “act forcefully” if needed. The FTSE 100 fell by more than 3 per cent yesterday and other markets around the world fell too as traders reacted to a notable change in tone from the Bank on tackling inflation. As a consequence, financial markets are now betting that the Bank will increase interest rates by 0.5 percentage points at its next three meetings and that the base rate will be more than 3 per cent by the end of the year.

The reasons for this change of tone can be linked to the feedback from the agents, who appear to have painted a picture of a UK economy which is holding up better than feared across the country but where rising prices are a problem.

These are extracts from the minutes of the MPC meeting about the agents’ feedback:

Intelligence from the Bank’s Agents suggested that, although there had been some early signs of a slowing in underlying growth, demand had remained mostly robust and broadly in line with projections at the time of the May Report

According to contacts of the Bank’s Agents, growth had continued to be held back by supply chain disruptions, although companies were increasingly taking measures to alleviate the effects of these disruptions, for example by using alternative inputs and holding more stock.

Intelligence from the Bank’s Agents’ contacts suggested that hiring intentions had continued to be positive and that recruitment difficulties had remained severe. Contacts had said that they expected recruitment difficulties to persist for at least the next twelve months, due to structural shortages of labour and skills

The Bank’s Agents had reported that pay settlements continued to be much higher than a year ago, with deals averaging just over 5%, a little above the 4.8% expected by companies in the Agents’ pay survey conducted near the beginning of this year. A significant minority of companies were considering mid-year top-ups to pay settlements. This recent intelligence reinforced the upside risk to the MPC’s central projections for pay growth and domestic price pressures highlighted in the May Report.

This stance is reflected in the scores the agents gave in their latest survey. They are asked to give scores of between -5 and +5 to judge parts of the economy compared to a year ago. The value of sales of goods and services was scored at 4 while manufacturing output was 1 and construction 2. The pressure on costs was demonstrated by scores of 5 for material costs and 4 for labour costs. Profit margins came in at -2 (although this metric has never been positive since it started in 2017) and recruitment difficulties were scored at 4. However, of the 22 scores provided, only two had got worse since the last report in April. These were business investment intentions, which fell from 3 to 2, and credit availability for large businesses, which fell from 2 to 1.

This all suggests that the evidence on the ground is that the economy is holding up better than the worst fears at the moment, paving the way for the Bank to tackle inflation more aggressively. The Bank published its quarterly update on the agent’s summary of business conditions alongside the minutes. It included this snippet on the broad state of demand:

Agency contacts in some sectors, such as business services as well as some manufacturers, continued to report strong demand, with output growth constrained by shortages of goods and labour. However, there were also signs of squeezed household real incomes starting to weigh on demand, for example for consumer goods and for house purchases.

While this is broadly positive, that point on consumer goods and house purchases feeling the impact of squeezed household incomes obviously has the potential to spiral into something much worse. The housing market is difficult to track in real-time due to sales going through months after they were initially agreed. However, it is difficult to see how rising mortgage costs and squeezed household income do not combine to deliver a blow to house prices. House price affordability has spiralled in England to 9.1 times annual average earnings but has been supported by historically cheap mortgages filling that gap. That support is now disappearing. The anecdotal evidence around us in East London is that sellers now face getting offers that are as much as 10 per cent less than could earlier in the year, with an increase in supply also impacting the market.

The challenge for economists in getting to the bottom of what is going on is significant. I was fascinated by the profit warning from Asos, which led to shares in the online fashion retailer falling more than 30 per cent yesterday. It demonstrated the different factors that are in play when trying to judge the mood of consumers. In a trading update for the three months to the end of May it said that net sales “were impacted by a significant increase in returns rates in the UK and Europe towards the end of the period, reflecting inflationary pressures on consumers which has a disproportionate impact on profitability”.

Asos’s returns have traditionally run at around a third, with younger shoppers now very much in the habit of buying five items of clothing and sending four back (for free) once they have tried them on at home. The company blamed the rise in returns in recent weeks on customers looking at their bank balance and deciding they can’t actually afford the clothes. Boohoo, Asos’s rival, issued a similar warning on returns, but for different reasons. Boohoo boss John Lyttle told Reuters:

“Through the pandemic we were all wearing athleisure, looser fitting, less fit sensitive, and now we're clearly back to dresses and particularly occasion dresses tend to be a little bit more fitted. So you have a higher return rate coming with that change from athleisure into dresses."

Other retailers have started charging for returns to try to offset the cost of dealing with unwanted items and try to discourage consumers from buying and then returning. However, for Asos and Boohoo it is a core part of their offer to younger shoppers.

For the economy, it’s a type of behaviour from consumers that is different to previous downturns. Hopefully the Bank’s agents are on top of it…

A chart that helps you understand the world

The FTSE 100 is on course to end the week down around 3 per cent, its biggest drop since the start of March, due to concerns about an economic slowdown and central banks increasing interest rates quickly to counter rising inflation. But not all companies suffer in this environment. A collection of FTSE 100 companies have actually risen this week, and this is them, courtesy of Refinitiv. They include HSBC, one of the UK’s biggest mortgage lenders…

You should also read this

One billion users, working from the office and no evidence of alien life. A summary of Elon Musk’s meeting with Twitter staff (Platformer)

I enjoyed this piece on contrarian investing from Tom Stevenson, investment director at Fidelity International and a regulator Telegraph columnist. It is headlined: “You can get rich on a falling stock market - if you have the stomach for it”. He notes that much of the coverage of markets falling is “written from the perspective of people who already own assets”, adding: “But it could just as easily be seen as an opportunity.” Stevenson runs through some of the cognitive biases in humans that make contrarian investing attractive (we over-emphasise negative events, for instance) and in general provides a beginners guide on where to start in this market… (Telegraph)

Dan McCrum, the FT journalist who covered the unravelling of German tech company Wirecard, on why fraudsters get away with it for so long (FT, paywall)

A look at Andy Jassy’s first year as Amazon boss after succeeding Jeff Bezos (WSJ, paywall)

A shortage of Sriracha sauce is coming after the leading US manufacturer Huy Fong Foods stopped production following a poor chilli harvest (Quartz)

Google Maps is going to start showing live traffic through a new widget (Tech Crunch)

And finally…

I have just finished The Premonition by Michael Lewis, which tells the story of a handful of medics and scientists in the US who separately worked on drawing up a plan for how to deal with a pandemic in the years before Covid-19 struck. When the virus does arrive, their work disappears into a mix of chaos and politics. It’s a fascinating read, even if you are bored of Covid. Lewis is brilliant at telling people’s stories, particularly those battling the establishment, as shown by his previous books like Moneyball and The Big Short. There are loads of useful takeaways in this book for business leaders, politicians, everyone really. For instance, the best insight about what is actually going on in an organisation can often be found well down the hierarchy (the L6 - level 6 - as Lewis describes it). Also, there is a big difference between having a plan and a purpose and actually practically enforcing it. Thirdly, the US may be progressive in many ways, but it is backwards and dysfunctional in many others, such as its public institutions. Finally, and most broadly, history is not certain - the Covid-19 crisis did not need to play out the way it did, or even happen at all. You can buy the book here.

Thanks for reading. Off to Lunch will be back on Sunday with our review of what’s interesting in the Sunday papers. Until then, enjoy your weekend. If you are enjoying Off to Lunch, then please spread the word

Graham