Have markets underestimated Covid?

...just look at Apple, Amazon and AO World

It feels odd to question whether markets have underestimated a global pandemic. But looking at the results from Apple, Amazon and Robinhood overnight, AO World in the UK this morning and the share price reactions that have followed, it is fair to ask. There are two areas where markets may have underestimated the impact of Covid – how much the pandemic is still disrupting supply chains and how much lockdowns temporarily changed consumer behaviour (rather than it being driven by the brilliance of businesses).

Apple warned last night that it faces a hit of between $4 billion and $8 billion to revenues in the second quarter of 2022 due to its suppliers in China being disrupted by Covid lockdowns, as well as the impact of the war in Ukraine. This led to Apple shares falling more than 4 per cent in after-hours trading despite stellar figures for the first quarter of 2022 (revenues up 9 per cent to $97.3 billion, ahead of forecasts). On Apple’s earnings call last night Tim Cook, the chief executive, appeared to suggest the company is more worried about supply chain disruption than the mood of consumers right now. When asked by an analyst whether Apple thought the cost-of-living squeeze will stop consumers buying its products, Cook replied:

“Well we're monitoring that closely, but right now our main focus, frankly speaking, is on the supply side.”

We flagged in last Friday’s Off to Lunch that Nikkei was reporting half of Apple’s suppliers are in areas hit by lockdown. Now Apple has put a number on the disruption and Cook has spoken about it.

The problem for Amazon is different. It has not been able to sustain the growth in online sales it enjoyed during the pandemic. It reported its smallest year-on-year rise in revenue for 20 years last night (7 per cent, which compares to 44 per cent in the same quarter last year). The number of products it sold was actually flat year-on-year and the company also posted its first quarterly loss since 2015. Shares in Amazon are going to fall around 10 per cent when markets open in the US. Brian Olsavsky, Amazon’s chief financial officer, said the company effectively has too much warehouse space and too many staff after expanding during the pandemic.

“We hired more people and then found ourselves overstaffed when the Omicron variant subsided rather quickly, at least from our standpoint in warehouses. So, the issue is switched from disruption to productivity losses to overcapacity on labour.”

As Richard Fletcher, my former boss at The Times, pointed out in his morning email today, these Amazon figures come on the back of Kantar reporting that online grocery sales in the UK are down 15 per cent year-on-year. The evidence is stacking up that the surge in online shopping during Covid is not going to stay at anything like the same level, with physical stores regaining share. Shares in AO World are down 20 per cent today after the Bolton-based online electrical retailer issued its third profit warning in six months. AO’s revenues are down 6 per cent year-on-year (albeit up 52 per cent compared to two years ago) and this share price graph tells its own story – the company’s Covid-19 boost has disappeared.

It is not just online shopping that has receded as the Covid-19 crisis has eased. Look at Netflix and streaming, Peloton and working-out at home, Robinhood and the frenzy in amateur share trading. Robinhood warned last night that its revenues were down 43 per cent year-on-year. Just look at its share price since floating last year:

People are getting back to how they behaved pre-Covid. Overall, that’s a good thing…

No further sales

Elon Musk has confirmed this morning that he has sold almost $4 billion of Tesla shares. Does this mean his $44 billion takeover of Twitter is a small step closer to becoming reality? Probably. But where does the other $17 billion of equity that he needs to do the deal come from? Other people and businesses? Tesla shares are up more than 3 per cent pre-market. Investors will be breathing a sigh of relief that Musk is not selling a bigger stake than this…

Where now for house prices?

House prices have risen less than economists expected in April, according to the latest survey from mortgage lender Nationwide. Prices are up by 0.3 per cent month-on-month in April, below the 0.8 per cent that economists had forecast, and 12.1 per cent year-on-year. This compares to the 1.1 per cent monthly growth and 14.3 per cent annual growth reported in March.

A cooling of the market in April seemed inevitable amid rising inflation and the prospect of higher interest rates making mortgages less affordable. Now the question is how much the market will cool. A good place to look for insight on this is Lloyds Banking Group, the UK’s biggest retail bank. The bank’s quarterly results on Wednesday included its assumptions for the UK economy, which underpin its financial outlook. For house prices, its base case is 3.3 per cent growth for 2022, 0 per cent for 2023 and 0.2 per cent for 2024. This is an upgrade since its full-year results in February, when Lloyds’ assumption was 0 per cent for 2022, 0 per cent for 2023 and 0.5 per cent for 2024.

One of the reasons that the market is likely to remain robust is the percentage of people looking to move. Nationwide published this graphic with its latest report:

A graph that helps you understand the world

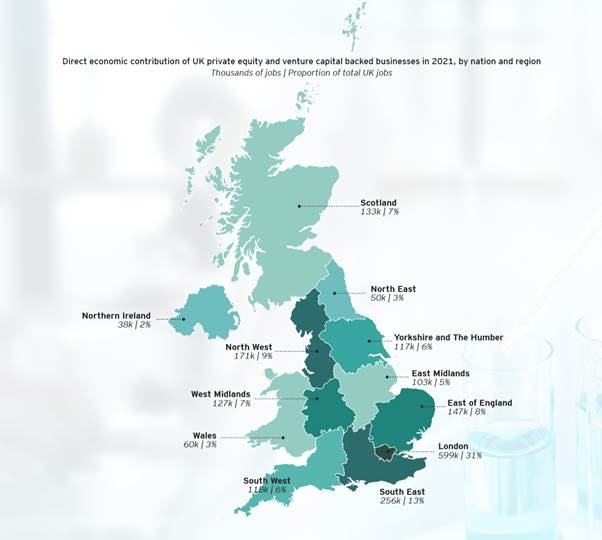

The trade body for private equity and venture capital firms has published a new report today designed to show the contribution of the industry to the UK economy. The report, produced by accountancy firm EY, is an attempt to boost the reputation of the private equity sector. It shows that two million jobs in the UK, more than half outside London and the south-east, are supported by private capital.

I spoke about the report this morning with Michael Moore, the director-general of the and commissioned by the British Private Equity & Venture Capital Association (who is a former Liberal Democrat MP and was Scotland secretary in the coalition government). “Our job is to show we are part of the mainstream and the UK economy – all of the UK economy, not just London and the south-east,” he said.

However, the BVCA’s attempts to boost the reputation of the sector hang on how the Issa brothers and TDR Capital manage Asda and how CD&R manages Morrisons. These two Yorkshire-based supermarkets are two of the UK’s biggest employers and account for hundreds of thousands of jobs. Moore defended their ownership so far, saying, for instance, that sale-and-leaseback deals are “not the unique preserve of the private equity industry”, with the government and other organisations doing them. He also pointed to the Issa brothers announcing last week that they were creating 32,000 jobs. Off to Lunch will be taking a deeper look at Asda and Morrisons soon…

You should also read this

A long read from the FT on the UK’s on-again, off-again attempts to attract investment from the crypto industry, which is not uniformly supported among the government and regulators (FT, £)

Plans for a new “Golden Valley” for cyber security next to GCHQ in Cheltenham are progressing…(Business Live)

….and property developers are planning to invest billions of dollars in labs and offices for the UK’s life sciences industry. This article includes an interesting quote from Michael Turner, president of Oxford Properties, the Canadian investor: “Brexit has led the UK through the 12 stages of grief . . . [but] the self-pity is overdone. It’s a good place to invest: well governed, with a good economy and rule of law.” (FT, £)

The role of value and momentum in sports betting and why punters would be better off investing their money in financial markets instead (Bloomberg, £)

And finally…

Elon Musk’s bid for Twitter and the varied business interests he now has got me thinking again about Range by David Epstein. This superb book explains why specialisation and relentlessly practising one skill is not the only route to success (a debate which started with Malcolm Gladwell’s 10,000-hour rule). One of the examples Epstein gives in the book is Roger Federer. The author explains how Federer played multiple sports when he was younger and only specialised in tennis as a teenager, which helps to explain his unique style and grace on a tennis court. Is this lack of specialisation one of the reasons for Musk’s unorthodox brilliance? This book is worth your time.

Thanks for reading. Please note, Off to Lunch will be back with you on Tuesday rather than Monday due to the bank holiday in the UK. If you want to contribute to the work of Off to Lunch, then please sign up for a paid subscription below. Alternatively, please just spread the word!

Graham